QUESTION IMAGE

Question

question 3

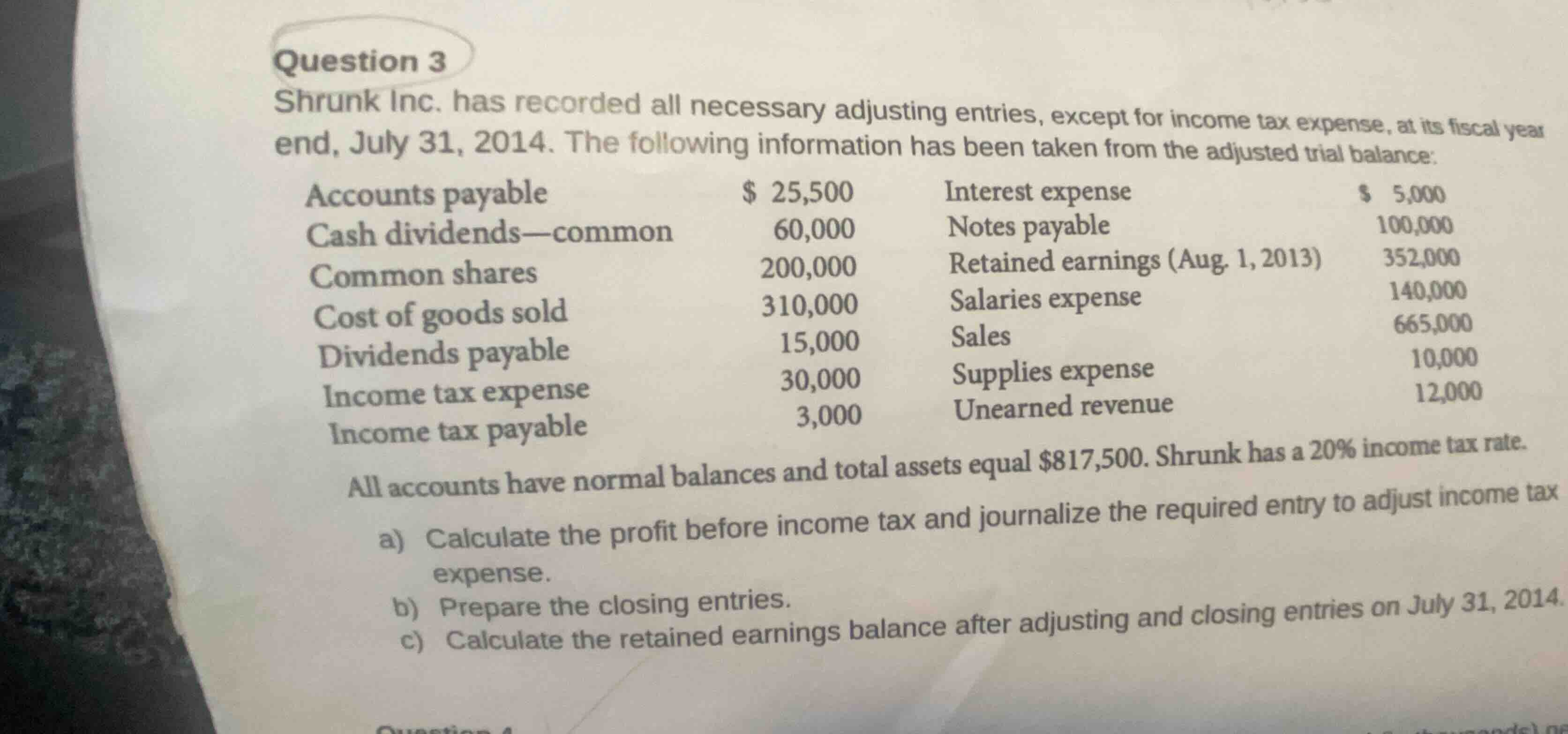

shrunk inc. has recorded all necessary adjusting entries, except for income tax expense, at its fiscal year end, july 31, 2014. the following information has been taken from the adjusted trial balance:

accounts payable: $ 25,500

cash dividends-common: 60,000

common shares: 200,000

cost of goods sold: 310,000

dividends payable: 15,000

income tax expense: 30,000

income tax payable: 3,000

interest expense: $ 5,000

notes payable: 100,000

retained earnings (aug. 1, 2013): 352,000

salaries expense: 140,000

sales: 665,000

supplies expense: 10,000

unearned revenue: 12,000

all accounts have normal balances and total assets equal $817,500. shrunk has a 20% income tax rate.

a) calculate the profit before income tax and journalize the required entry to adjust income tax expense.

b) prepare the closing entries.

c) calculate the retained earnings balance after adjusting and closing entries on july 31, 2014.

<pre_analysis>

{

"quality": "clear",

"question_count": 3,

"skills_matched": [

"step_cot",

"explain_then_answer",

"tutor"

],

"needs_drawing": false,

"concepts_used": [],

"new_concepts": [

"Adjusting Entries",

"Closing Entries",

"Retained Earnings Statement"

],

"current_concepts": [

"Adjusting Entries",

"Closing Entries",

"Retained Earnings Statement",

"Income Statement"

]

}

</pre_analysis>

<reasoning>

Calculate profit before income tax and journalize adjusting entry

To find the profit before income tax, we subtract all operating and non-operating expenses (excluding income tax expense) from revenues.

Revenues:

- Sales: \$665,000

Expenses (excluding income tax):

- Cost of goods sold: \$310,000

- Salaries expense: \$140,000

- Supplies expense: \$10,000

- Interest expense: \$5,000

Total expenses before tax:

\[

310,000 + 140,000 + 10,000 + 5,000 = 465,000

\]

Profit before income tax:

\[

665,000 - 465,000 = 200,000

\]

Next, we calculate the required income tax expense based on the 20% tax rate:

\[

200,000 \times 20\% = 40,000

\]

The trial balance currently shows an unadjusted balance for Income tax expense of \$30,000. To adjust it to the correct amount of \$40,000, we need an additional adjusting entry of:

\[

40,000 - 30,000 = 10,000

\]

The adjusting journal entry on July 31, 2014 is:

- Debit Income Tax Expense: \$10,000

- Credit Income Tax Payable: \$10,000

Prepare the closing entries

Closing entries transfer temporary account balances (revenues, expenses, dividends) to Retained Earnings.

- Close revenue accounts to Income Summary:

- Debit Sales: \$665,000

- Credit Income Summary: \$665,000

- Close expense accounts (including the adjusted income tax expense of \$40,000) to Income Summary:

- Debit Income Summary: \$505,000

- Credit Cost of Goods Sold: \$310,000

- Credit Salaries Expense: \$140,000

- Credit Supplies Expense: \$10,000

- Credit Interest Expense: \$5,000

- Credit Income Tax Expense: \$40,000

- Close Income Summary (representing net income of \$160,000) to Retained Earnings:

- Debit Income Summary: \$160,000

- Credit Retained Earnings: \$160,000

- Close Dividends to Retained Earnings:

- Debit Retained Earnings: \$60,000

- Credit Cash Dividends—Common: \$60,000

Calculate the ending retained earnings balance

We calculate the ending balance of Retained Earnings on July 31, 2014, using the beginning balance, net income, and dividends:

- Beginning Retained Earnings (Aug. 1, 2013): \$352,000

- Add: Net Income: \$160,000

- Less: Cash Dividends—Common: \$60,000

Ending Retained Earnings:

\[

352,000 + 160,000 - 60,000 = 452,000

\]

</reasoning>

<answer>

Question 3

a) Profit Before Income Tax and Adjusting Entry

- Profit before income tax: \$200,000

- Required Income Tax Expense (20%): \$40,000

- Adjusting Journal Entry (July 31, 2014):

| Date | Account Titles | Debit | Credit |

|---|---|---|---|

| Income Tax Payable | \$10,000 |

---

b) Closing Entries (July 31, 2014)

- To close revenue:

- Debit: Sales \$665,000

- Credit: Income Summary \$665,000

- To close expenses:

- Debit: Income Summary \$505,000

- Credit: Cost of Goods Sold \$310,000

- Credit: Salaries Expense \$140,000

- Credit: Supplies Expense \$10,000

- Credit: Interest Expense \$5,000

- Credit: Income Tax Expense \$40,000

- To close net income to retained earnings:

- Debit: Income Summary \$160,000

- Credit: Retained Earnings \$160,000

- **To close divide…

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

<pre_analysis>

{

"quality": "clear",

"question_count": 3,

"skills_matched": [

"step_cot",

"explain_then_answer",

"tutor"

],

"needs_drawing": false,

"concepts_used": [],

"new_concepts": [

"Adjusting Entries",

"Closing Entries",

"Retained Earnings Statement"

],

"current_concepts": [

"Adjusting Entries",

"Closing Entries",

"Retained Earnings Statement",

"Income Statement"

]

}

</pre_analysis>

<reasoning>

Calculate profit before income tax and journalize adjusting entry

To find the profit before income tax, we subtract all operating and non-operating expenses (excluding income tax expense) from revenues.

Revenues:

- Sales: \$665,000

Expenses (excluding income tax):

- Cost of goods sold: \$310,000

- Salaries expense: \$140,000

- Supplies expense: \$10,000

- Interest expense: \$5,000

Total expenses before tax:

\[

310,000 + 140,000 + 10,000 + 5,000 = 465,000

\]

Profit before income tax:

\[

665,000 - 465,000 = 200,000

\]

Next, we calculate the required income tax expense based on the 20% tax rate:

\[

200,000 \times 20\% = 40,000

\]

The trial balance currently shows an unadjusted balance for Income tax expense of \$30,000. To adjust it to the correct amount of \$40,000, we need an additional adjusting entry of:

\[

40,000 - 30,000 = 10,000

\]

The adjusting journal entry on July 31, 2014 is:

- Debit Income Tax Expense: \$10,000

- Credit Income Tax Payable: \$10,000

Prepare the closing entries

Closing entries transfer temporary account balances (revenues, expenses, dividends) to Retained Earnings.

- Close revenue accounts to Income Summary:

- Debit Sales: \$665,000

- Credit Income Summary: \$665,000

- Close expense accounts (including the adjusted income tax expense of \$40,000) to Income Summary:

- Debit Income Summary: \$505,000

- Credit Cost of Goods Sold: \$310,000

- Credit Salaries Expense: \$140,000

- Credit Supplies Expense: \$10,000

- Credit Interest Expense: \$5,000

- Credit Income Tax Expense: \$40,000

- Close Income Summary (representing net income of \$160,000) to Retained Earnings:

- Debit Income Summary: \$160,000

- Credit Retained Earnings: \$160,000

- Close Dividends to Retained Earnings:

- Debit Retained Earnings: \$60,000

- Credit Cash Dividends—Common: \$60,000

Calculate the ending retained earnings balance

We calculate the ending balance of Retained Earnings on July 31, 2014, using the beginning balance, net income, and dividends:

- Beginning Retained Earnings (Aug. 1, 2013): \$352,000

- Add: Net Income: \$160,000

- Less: Cash Dividends—Common: \$60,000

Ending Retained Earnings:

\[

352,000 + 160,000 - 60,000 = 452,000

\]

</reasoning>

<answer>

Question 3

a) Profit Before Income Tax and Adjusting Entry

- Profit before income tax: \$200,000

- Required Income Tax Expense (20%): \$40,000

- Adjusting Journal Entry (July 31, 2014):

| Date | Account Titles | Debit | Credit |

|---|---|---|---|

| Income Tax Payable | \$10,000 |

---

b) Closing Entries (July 31, 2014)

- To close revenue:

- Debit: Sales \$665,000

- Credit: Income Summary \$665,000

- To close expenses:

- Debit: Income Summary \$505,000

- Credit: Cost of Goods Sold \$310,000

- Credit: Salaries Expense \$140,000

- Credit: Supplies Expense \$10,000

- Credit: Interest Expense \$5,000

- Credit: Income Tax Expense \$40,000

- To close net income to retained earnings:

- Debit: Income Summary \$160,000

- Credit: Retained Earnings \$160,000

- To close dividends:

- Debit: Retained Earnings \$60,000

- Credit: Cash Dividends—Common \$60,000

---

c) Retained Earnings Balance (July 31, 2014)

- Ending Retained Earnings Balance: \$452,000

</answer>

<post_analysis>

{

"subject": "Business",

"question_type": "Multi-part",

"knowledge_point": [

"Business",

"Accounting",

"Adjusting and Closing Entries"

]

}

</post_analysis>