QUESTION IMAGE

Question

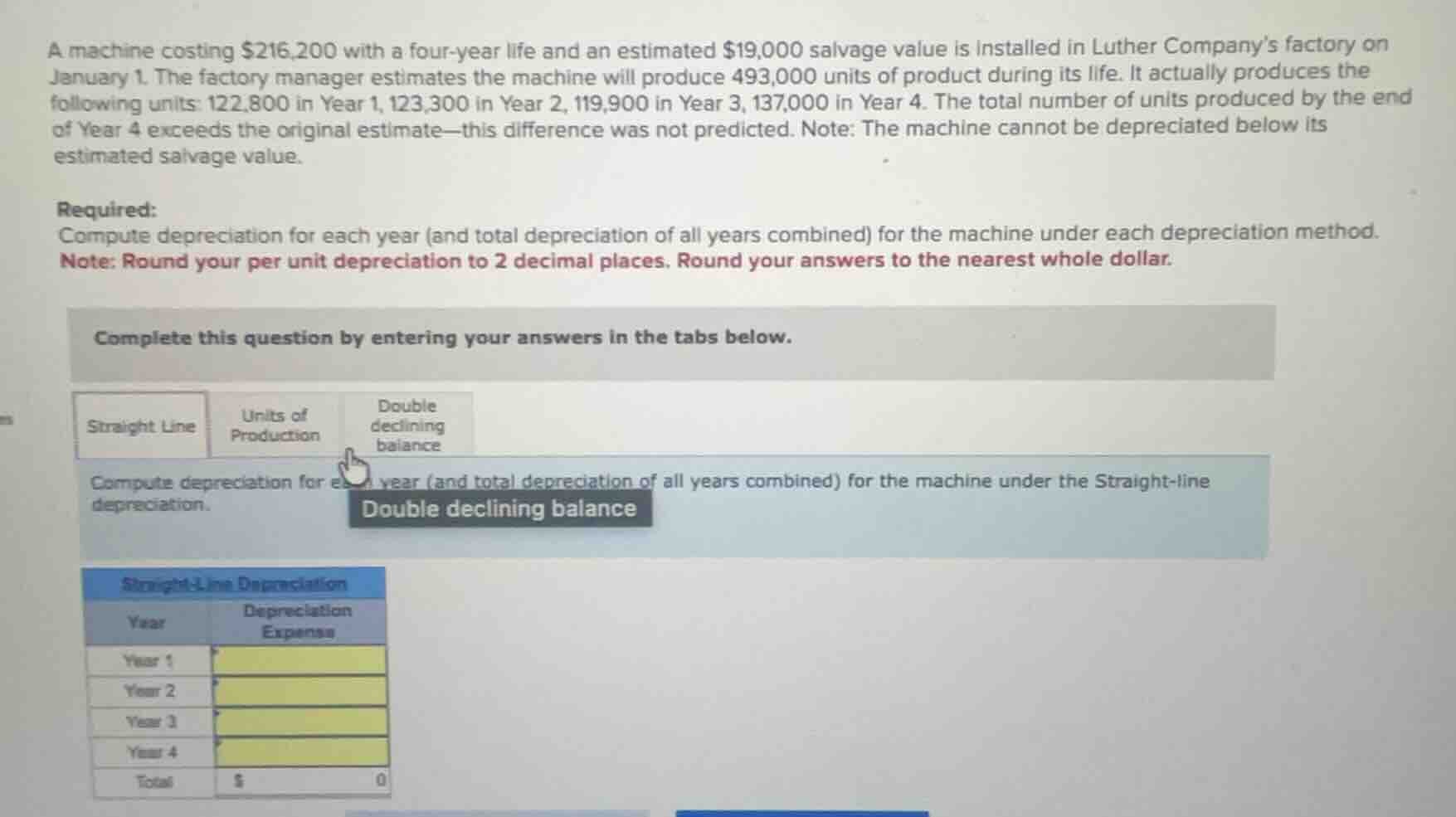

a machine costing $216,200 with a four-year life and an estimated $19,000 salvage value is installed in luther company’s factory on january 1. the factory manager estimates the machine will produce 493,000 units of product during its life. it actually produces the following units: 122,800 in year 1, 123,300 in year 2, 119,900 in year 3, 137,000 in year 4. the total number of units produced by the end of year 4 exceeds the original estimate—this difference was not predicted. note: the machine cannot be depreciated below its estimated salvage value.

required:

compute depreciation for each year (and total depreciation of all years combined) for the machine under each depreciation method.

note: round your per unit depreciation to 2 decimal places. round your answers to the nearest whole dollar.

complete this question by entering your answers in the tabs below.

straight line units of production double declining balance

compute depreciation for each year (and total depreciation of all years combined) for the machine under the straight-line depreciation. double declining balance

straight-line depreciation

year depreciation expense

year 1

year 2

year 3

year 4

total $ 0

Straight - Line Depreciation

Step 1: Calculate Depreciable Cost

The depreciable cost is the cost of the asset minus the salvage value. The formula for depreciable cost is \( \text{Depreciable Cost}=\text{Cost}-\text{Salvage Value} \).

Given that the cost of the machine is \( \$216,200 \) and the salvage value is \( \$19,000 \), we have:

\( \text{Depreciable Cost}=216200 - 19000=\$197200 \)

Step 2: Calculate Annual Depreciation

The straight - line depreciation formula is \( \text{Annual Depreciation}=\frac{\text{Depreciable Cost}}{\text{Useful Life}} \).

The useful life of the machine is 4 years. So,

\( \text{Annual Depreciation}=\frac{197200}{4}=\$49300 \)

Since the straight - line depreciation is the same for each year (as long as the asset is not depreciated below salvage value, and in this case, the annual depreciation does not cause that), the depreciation expense for each of the 4 years is \( \$49300 \).

Step 3: Calculate Total Depreciation

The total depreciation over 4 years is the sum of the annual depreciation for each year. Since each year's depreciation is \( \$49300 \), the total depreciation is \( 49300\times4=\$197200 \) (which should also equal the depreciable cost, as a check).

Step 1: Calculate Depreciation per Unit

The formula for depreciation per unit is \( \text{Depreciation per Unit}=\frac{\text{Depreciable Cost}}{\text{Estimated Total Units of Production}} \).

We know that the depreciable cost is \( \$197200 \) (from the straight - line calculation) and the estimated total units of production is 493,000 units.

\( \text{Depreciation per Unit}=\frac{197200}{493000}\approx\$0.40 \) (rounded to 2 decimal places)

Step 2: Calculate Depreciation for Each Year

- Year 1: Units produced = 122,800. Depreciation expense = \( 122800\times0.40=\$49120 \)

- Year 2: Units produced = 123,300. Depreciation expense = \( 123300\times0.40=\$49320 \)

- Year 3: Units produced = 119,900. Depreciation expense = \( 119900\times0.40=\$47960 \)

- Year 4: First, we need to find out how many units we can depreciate for. The total depreciable units (to reach salvage value) is 493,000. The sum of units produced in the first 3 years is \( 122800 + 123300+119900 = 366000 \) units. So the number of units we can depreciate in Year 4 is \( 493000 - 366000=127000 \) units (we use this instead of the actual 137,000 units because we can't depreciate below salvage value).

Depreciation expense for Year 4 = \( 127000\times0.40=\$50800 \) (Wait, but let's check: The depreciable cost is \( \$197200 \). The sum of depreciation for Year 1, Year 2, Year 3 is \( 49120 + 49320+47960 = 146400 \). So the remaining depreciable amount is \( 197200 - 146400 = 50800 \), which matches. If we used 137,000 units, the depreciation would be \( 137000\times0.40 = 54800 \), but \( 146400+54800=201200 \), which is more than the depreciable cost of \( 197200 \), so we use the number of units that brings the total depreciation to the depreciable cost.

Step 3: Calculate Total Depreciation

The total depreciation is the sum of the depreciation for each year: \( 49120+49320 + 47960+50800=\$197200 \)

Step 1: Calculate the Straight - Line Depreciation Rate

The straight - line depreciation rate is \( \frac{1}{\text{Useful Life}}\times100\% \). For a 4 - year life, the straight - line rate is \( \frac{1}{4}\times100\% = 25\% \).

The double - declining - balance rate is twice the straight - line rate, so \( 2\times25\%=50\% \)

Step 2: Calculate Depreciation for Each Year

- Year 1:

The book value at the beginning of Year 1 is the cost of the asset, \( \$216,200 \).

Depreciation expense for Year 1 = \( \text{Book Value at Beginning of Year}\times\text{Double - Declining Rate} \)

\( \text{Depreciation Year 1}=216200\times0.5=\$108100 \)

Book value at the end of Year 1 = \( 216200 - 108100=\$108100 \)

- Year 2:

Depreciation expense for Year 2 = \( 108100\times0.5=\$54050 \)

Book value at the end of Year 2 = \( 108100 - 54050=\$54050 \)

- Year 3:

Depreciation expense for Year 3 = \( 54050\times0.5=\$27025 \)

Book value at the end of Year 3 = \( 54050 - 27025=\$27025 \)

- Year 4:

We need to ensure that we do not depreciate below the salvage value of \( \$19,000 \). The book value at the beginning of Year 4 is \( \$27025 \). The depreciation expense for Year 4 is \( 27025 - 19000=\$8025 \) (because if we used the double - declining rate, the depreciation would be \( 27025\times0.5 = 13512.5 \), but that would make the book value \( 27025-13512.5 = 13512.5 \), which is below the salvage value of \( \$19,000 \). So we depreciate only up to the salvage value).

Step 3: Calculate Total Depreciation

Total depreciation = Depreciation Year 1+Depreciation Year 2+Depreciation Year 3+Depreciation Year 4

\( = 108100+54050 + 27025+8025=\$197200 \)

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

- Year 1 Depreciation Expense: \( \$49300 \)

- Year 2 Depreciation Expense: \( \$49300 \)

- Year 3 Depreciation Expense: \( \$49300 \)

- Year 4 Depreciation Expense: \( \$49300 \)

- Total Depreciation: \( \$197200 \)